The Start of the Year

Estimated reading time: 0 minutes

Ready, Set, Go!

A new year is underway and it feels good to be back. The beginning of the year in markets is always an exciting time because so much lies ahead of us. The unpredictability of it almost seems welcome, investors aren’t yet jaded by surprises or finding out their expectations were off-base.

January is fun. And it’s especially fun after a killer year-end rally that made many account balances fatter and happier.

The question to then ask is this: What happens after a really strong year in markets? The S&P finished 2023 up 24%, which is well above average and especially surprising considering how bearish sentiment was to start the year. We can never know what a year may hold, but here’s a look at the average historical experiences.

Frankly, these all look pretty good and I’d be happy with a 9-10% return in any year when recession risks were elevated, 2024 included. The problem with long-term averages is that the actual outcome rarely lines up with the average. Which means the message here is if you’re a long-term investor, the moves that happen over a one month or one quarter, or sometimes even one year period matter much less. What matters is being invested for the long haul… but we already knew that.

So why bother trying to figure out what the average experience is after a big year? In many respects, I’d say there’s little value in exercises like this, yet we will continue to do them every year. It keeps us entertained, I suppose.

What they may be useful for is gauging the risk level and understanding the odds of a repeat experience. In summary, the year after a big up year can be expected to be more muted than average, which I’d translate to: The chances of having another double digit positive return are low, but that doesn’t mean we’ll have a down year. Even more simply put, extreme scenarios don’t usually repeat.

Insanity

The famous quote goes “The definition of insanity is doing the same thing over and over and expecting different results.” We could apply that to a lot of different things in markets today, but I’m choosing to apply it here with monetary policy.

If we hike rates quickly and by a large amount, but expect the result to be a painless soft landing that includes expanding profit margins, low unemployment, and a healthy inflation situation… that tells me we’re doing something we’ve done before (hiked rates), but we’re expecting different results.

The results may in fact be different from prior cycles, but I still expect them to be different in the form of the reaction function of markets and economic data, not different in the form of contraction/no contraction.

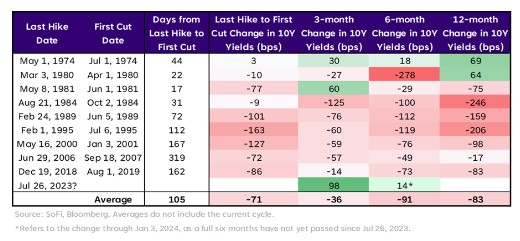

Who Knows First?

It’s long been a loose belief that the bond market knows things before the stock market. We could probably debate if that’s still the case, but one thing I’m still relatively confident in is that when the 10-year yield drops (and conversely, the price rises), it doesn’t typically signal rainbows and unicorns.

Since October 31, the 10-year Treasury yield is down 98 bps. Much of that is due to cooler inflation prints and a so-called Fed pivot.

The period between the end of hikes and the beginning of cuts does typically include a drop in 10-year yields. Interestingly in this cycle, during the three and six month* periods following the last hike — if that was in fact on July 26, 2023 — the 10-year yield has actually risen.

We could interpret that as a sign of economic strength that reduces our fears of recession, but that may be misguided. For context, the only time in history when 10-year yields rose through a hike-to-cuts transition was in the mid-70s. That period was during a recession, when oil prices had risen substantially, CPI was running at 10%, and the economy was struggling with stagflation. Inflation was clearly not under control, and that scenario is very different from what we’re experiencing now.

As such, if 10-year yields do not experience a more prolonged drop, it would be the first time in history when that happened (see insanity section above). And the only reference we have for when yields rose is not a period we want to repeat.

Uncertainty still abounds in 2024, and rate cuts are likely on the agenda. Treasury yields seem likely to fall on the short end of the curve as a result, but the 10-year yield is a big question — and one that could look very different from 2023. If that’s the case, stocks are likely to look very different from 2023 as well.

Here’s to another year of navigating the market seas.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, investment advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.