The 2025 Outlook

Estimated reading time: 0 minutes

Defying Gravity

Gravity can be defined as a force that pulls two objects with mass toward each other, or more commonly, the force that makes things fall to the ground. Throughout the bull market of the past two years, there have been many forces that could have, and perhaps should have, acted as a gravitational force on markets — yet major stock indices rose to new all-time highs and defied gravity.

The debate over whether we’ll have a soft landing or hard landing has shifted — we’re now debating just how soft the landing will be, or whether there will be a landing at all. Hard landing narratives have left the chat, and optimism has permeated investor sentiment. Those trends were mostly in place before the U.S. presidential election, and have been fueled even more since then as we learn just how powerful political forces can be.

The New Year is an opportunity to start fresh and see our portfolios with new eyes. Of course, we always need to be aware of the risks, but we can’t invest by waiting for historical precedent to repeat in the same ways it has before. I, for one, have had to learn that lesson over and over throughout this cycle, as history has been a poor guide for what’s transpired. The trends remain strong, the economy has stayed on stable footing; and perhaps most importantly for markets, the buyers are still buying. For now — don’t fight it, ride it.

The Roar of 2024

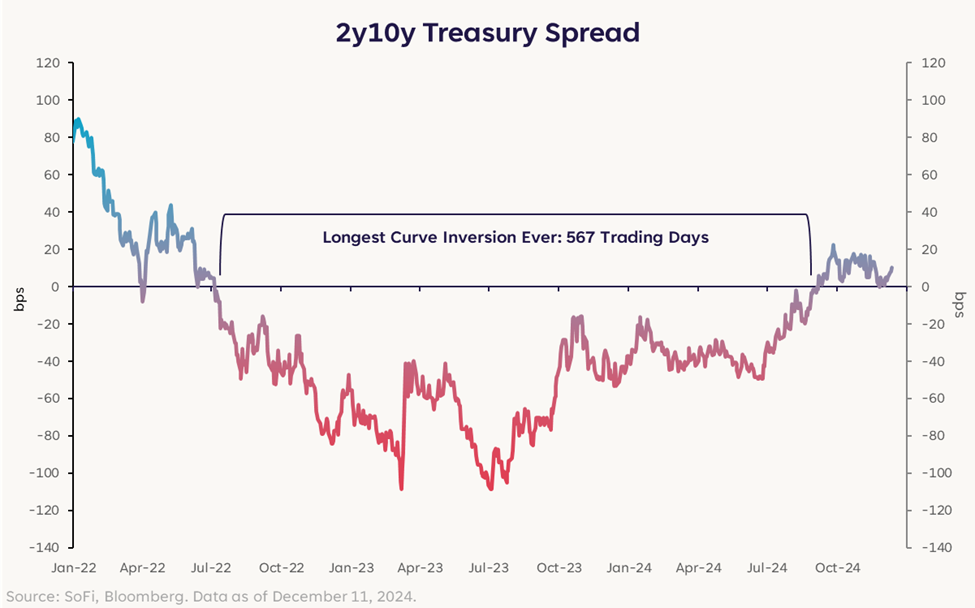

The past year brought with it the beginning of the Federal Reserve’s rate cutting cycle, the continuation of an AI-fueled rally, an unemployment rate that rose above 4% for the first time since 2021, a wild election cycle, a Japanese currency scare, and a Treasury yield curve that finally re-steepened after its longest inversion ever.

Despite all the drama, the S&P 500’s biggest pullback for the year was 8.5%, considerably less than the average intra-year drawdown of 13%. A post-election relief and risk-on rally drove markets even higher, pushing the idea of a pullback even further from investors’ minds.

Nevertheless, there were a few noteworthy stocks that saw intra-year drawdowns much larger than that: Nvidia (-27%), Tesla (-43%), Super Micro Computer (-85%), and Dollar General (-55%). With the exception of Dollar General, all of those stocks are strongly positive year-to-date, showing how much price volatility there’s been this year.

The AI theme continued to power markets forward as the potential for increased productivity and innovation kept momentum intact. That said, the pace did slow as the year progressed, with investors increasingly looking for margin expansion and tangible profit to justify the large amounts of spending that has been directed toward AI. This resulted in a rotation into other areas of tech (i.e. software, but more on that later) and across different parts of the equity universe as investors search for other growth opportunities.

As for bond markets, the most notable aspect of 2024 was how much Treasury yields moved, with the 2-year yield surpassing 5% in late April, only to fall 150 basis points by the end of September. The 10-year saw similarly huge moves throughout the year, and the spread between the 2- and 10-year yield turned positive (i.e. un-inverted) for the first time since July 2022.

Contrary to conventional wisdom, stock market performance has been relatively unperturbed by the yield curve volatility, leading pundits to increasingly dismiss the shape of the curve as a useful indicator of anything ominous. I am not convinced that it should be ignored.

The persistence of buying appetite, both from investors and consumers, has kept the bull market rolling. We enter the holiday season and a new year with very little gravity pulling us down.

Rolling Into the First Half of 2025

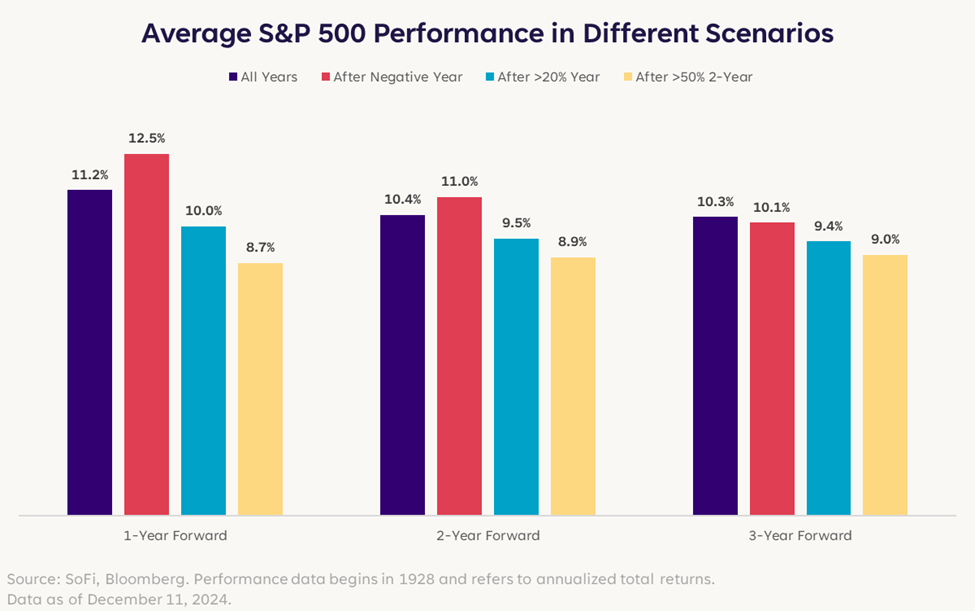

2025 could prove to be the third year of this bull market run, but the age of the bull market tells us very little about how long it may last. Throughout history, we’ve seen bull markets that lasted less than two years, and others that lasted longer than 10. Knowing that the S&P was up 26% in 2023 and is likely to finish 2024 near or above that mark, it’s easy to wonder if all the juice has already been squeezed out.

What we found, however, is that even after consecutive strong years, the market can still do well — maybe not >25% well, but high single digits to low double digits well. It’s important to note that on average the strongest performance comes after negative years, but the blue and yellow bars below do not ring any alarm bells.

Current index levels present valuation risks and investors should be prepared for a more muted year of returns relative to 2023 and 2024, but we believe 2025 will still present opportunities and new ways to put money to work. We expect four pillars to support markets in the first half of the New Year, suggesting a friendly environment for earnings growth, and one that carries forward the current optimistic economic and business sentiment.

Pillar #1: Liquidity Spigot

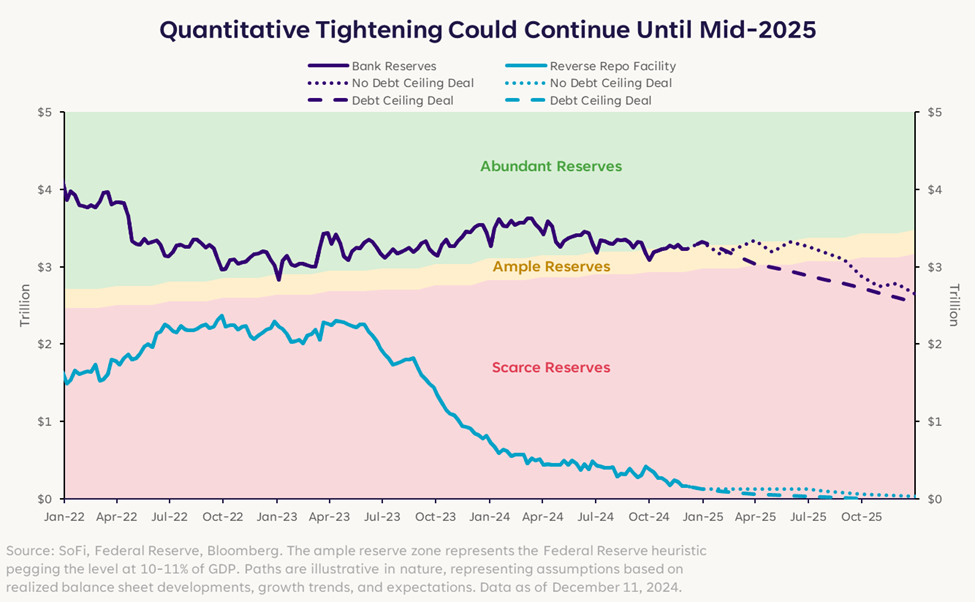

The year could get off to a raucous political start as the debt ceiling limit will be reinstated on January 1. Once that happens, the Treasury will not be able to issue new debt until Congress raises the ceiling, which we do not expect to happen with any quickness.

Fear not, there is money available in the Treasury General Account (TGA) to cover spending in the meantime. In fact, estimates suggest the Treasury will have enough financial flexibility to cover expenses until the summer… even more reason why raising the debt ceiling is not an immediate threat to markets.

This means a few things: 1) Even without new debt issuance, money from the TGA will effectively boost market liquidity, 2) these available funds allow the Fed to continue on its quantitative tightening (QT) path, theoretically until mid-2025, 3) despite QT, bank reserves are likely to remain above the “scarce” range until then, which quells liquidity concerns.

Markets like liquidity, and many would argue the rally we’ve seen since late 2022 has been driven at least in part by liquidity being pumped into the system. Conceptually, there could be harsh consequences of this (i.e. reigniting inflation, excess government debt burden, increased interest expense), but so far those have not come to pass. In the first half of 2025, liquidity is still expected to be flowing enough to support markets.

Pillar #2: Strong Labor => Productivity => Cooling Wage Pressure

For much of 2024, markets feared a weakening labor market that could come with layoff announcements and an unemployment rate rising to uncomfortable levels. Since “promote maximum employment” is one of the Fed’s two mandates, a weak labor market would have strongly influenced the rate path. Long story short, that didn’t happen.

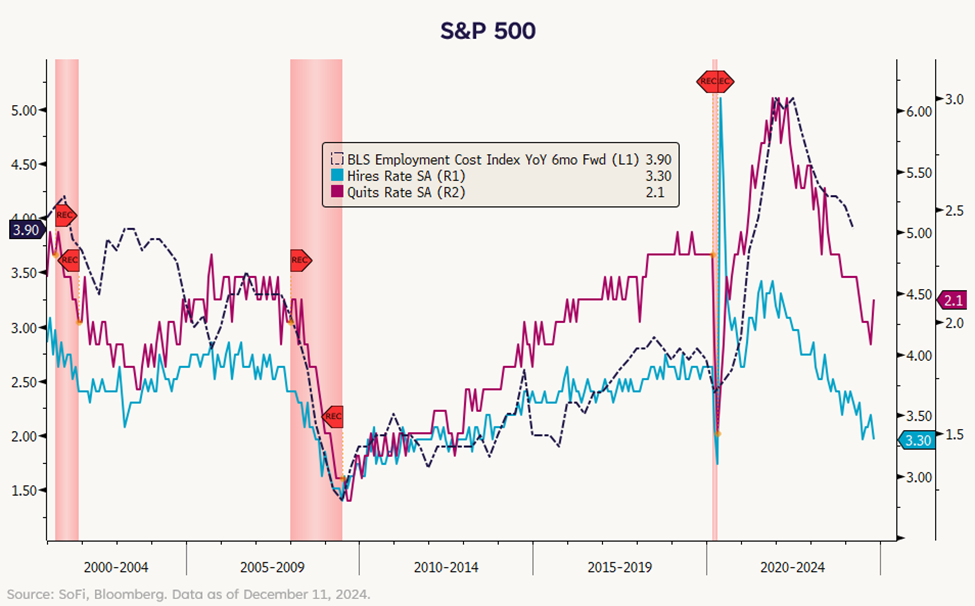

Instead, what we are in the midst of is a labor market that has slowed down and shown less churn, but remained stable and resilient. (By labor churn we mean things like the quits rate and the hires rate, both of which have declined steadily since 2022, but fell below pre-pandemic levels in 2024.)

The reason this matters is that it has helped reduce wage pressure that was fueling some inflation fears, and perhaps more importantly for 2025, because lower labor churn can power higher labor productivity. Fewer people moving around means people staying in jobs longer, which means a more efficient and productive workforce. In fact, current labor productivity is running slightly above 2%, which is higher than the non-recessionary average of about 1.4%. Higher productivity contributes to real growth in an economy.

Moreover, the chart below shows that measures of labor churn tend to lead wage costs by roughly six months. Since labor churn has fallen, we would expect wage costs (the dashed line) to continue falling as well.

As long as inflation remains under control or continues cooling, lower wage growth is not broadly detrimental to consumers. And if wage growth is falling, company labor costs are also coming down, putting less pressure on their bottom lines and allowing margins to stay stable or even expand. From an investor’s perspective, margins are critically important to earnings growth and return potential, so if this dynamic remains in place, it’s another supporting element for equity markets into 2025.

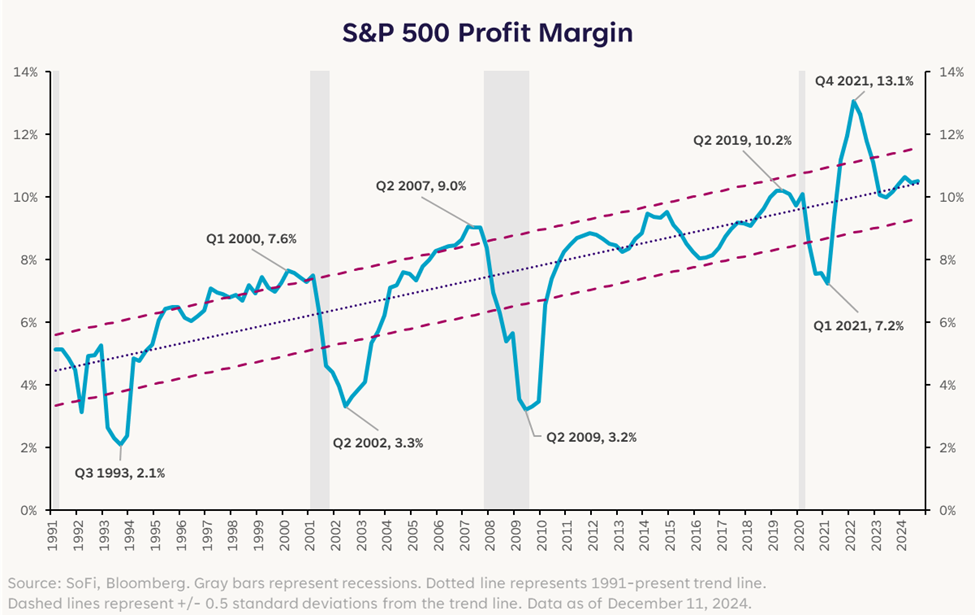

Profit margins for S&P 500 companies are currently running at trend, which is a healthy and balanced place to be, albeit lower than what we enjoyed between Q3 2021 and Q4 2022.

As an added tailwind, the new administration is expected to bring with it a looser regulatory regime, which could serve as a boost for industries such as financials, energy, and metals and mining, allowing for margins to expand.

Over time, we could also add AI and innovation to this supporting pillar as business innovation drives further productivity and profitability… but at this juncture that’s still a future force more than a current tangible reality.

Pillar #3: Inflation Under Control

We’ve come a long way from a Consumer Price Index (CPI) of 9.1% in June 2022 down to 2.7% for October 2024, which has calmed many anxieties. There are still elements of inflation that remain bothersome, namely shelter and car insurance, but many of the major components have cooled enough to satisfy markets.

The Fed’s preferred measure of inflation – the core Personal Consumption Index (PCE) – currently sits at 2.8%, down from a high of 5.6% in February 2022. Again, major progress has been made, and although not quite at the Fed’s 2% target, markets seem satisfied.

The important piece of this pillar is that inflation expectations stay under control, which could be tricky in 2025 with the prospect of increased tariffs and the level of optimism markets are exhibiting (see “What Could Go Wrong” later in this piece). This is perhaps the most questionable pillar in the pack, as inflation expectations have risen since late summer and the potential for the Fed to pause its rate cutting cycle has risen alongside.

We do expect the Fed to continue cutting rates, but at a much slower pace than originally thought. We also expect there to be adjustments made to the Fed’s projections on the neutral rate – not only the level, but the timeframe over which it may be met. If markets can remain comfortable with a higher neutral rate and a more gradual cutting cycle, inflation may not present too many problems.

In this case, the simple lack of a reignition in inflation would be a positive for markets.

Pillar #4: Sentiment has Momentum

Vibes are a powerful force for investor psychology, and although they are difficult to measure and can be fleeting, they are a force to be reckoned with when it comes to momentum. With the exception of a few blips here and there, market momentum and sentiment has been positive and pushing markets higher. We expect that trend to still have legs into 2025.

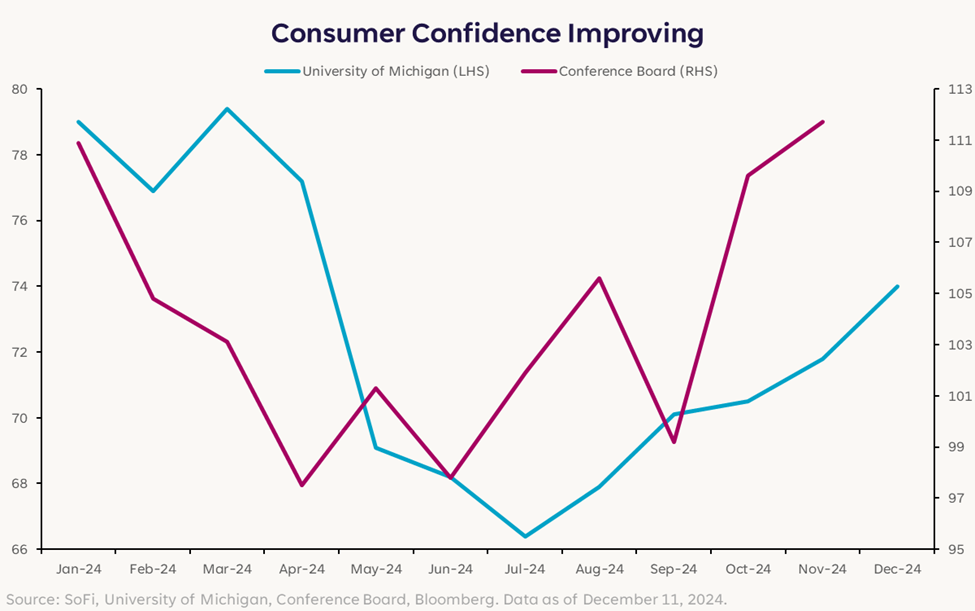

The main measures of consumer vibes are the sentiment surveys — namely, the Conference Board’s Consumer Confidence and the University of Michigan’s Consumer Sentiment surveys. In the first half of 2024, there were worries about higher than expected inflation and a slowing economy, which pushed both survey measures lower into summer. But there’s been reasonably steady improvement since then, which could continue if the labor market remains stable and the outlook for growth in 2025 stays strong. Watch for the trend to stay intact on both of these metrics.

Other major surveys that can give us a pulse on how businesses are feeling include the NFIB Small Business Optimism survey and the Purchasing Managers’ Index (PMI). These have also shown recent signs of improving, with November’s Small Business Optimism survey showing the largest single-month improvement in sentiment since July 1980.

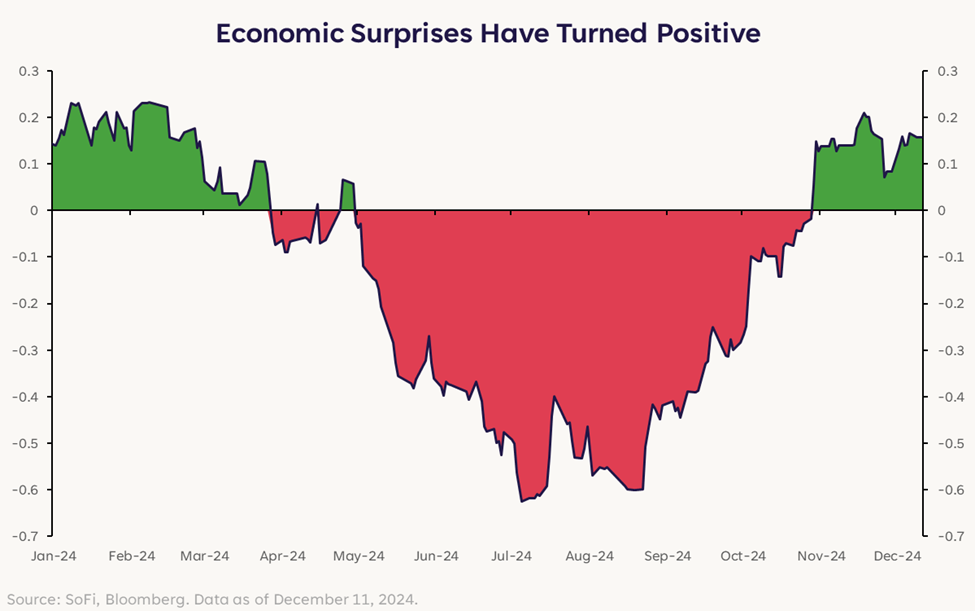

One of the clear signs of improvement over recent months has been the U.S. economic surprise index, as data pertaining to GDP growth, consumer spending, jobs, and inflation has generally come in better than feared.

Post-election, the combination of positive economic surprises, certainty around the election outcome, and the expectation of a friendlier regulatory and capital markets environment could drive business sentiment higher from here.

For small businesses, the level of interest rates will be critical to sentiment and a gradual move down would be helpful. For larger companies, tariffs and U.S. dollar strength are critical components to future prospects. We are keeping a close eye on all of these indicators for confirmation or denial of our sentiment thesis.

What it all means for Equities

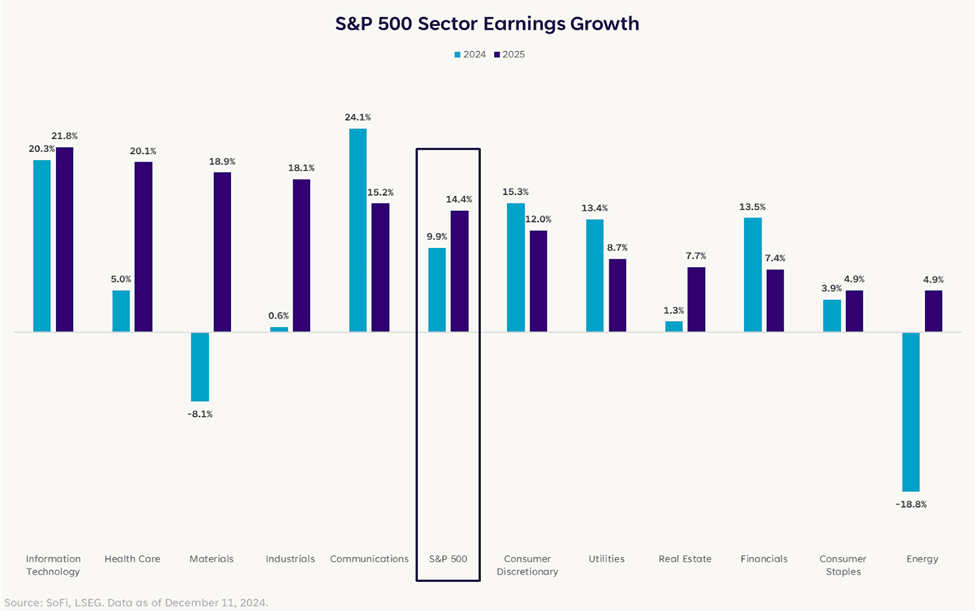

While sentiment and momentum can wield a lot of power, fundamentals are the key to market direction over longer term periods, which brings us to earnings. Earnings expectations for 2025 are strong – some might say too strong – but even if revised down slightly, companies still look to be in better shape than in 2024.

The drivers of earnings growth are important to note here. Technology is still at the top of the heap, but other sectors such as Health Care, Industrials, and Materials find themselves in new leadership positions if these forecasts come true. Also of note is that two of those three fall into the “cyclical” category and could be beneficiaries of the pro-growth sentiment that has materialized post-election.

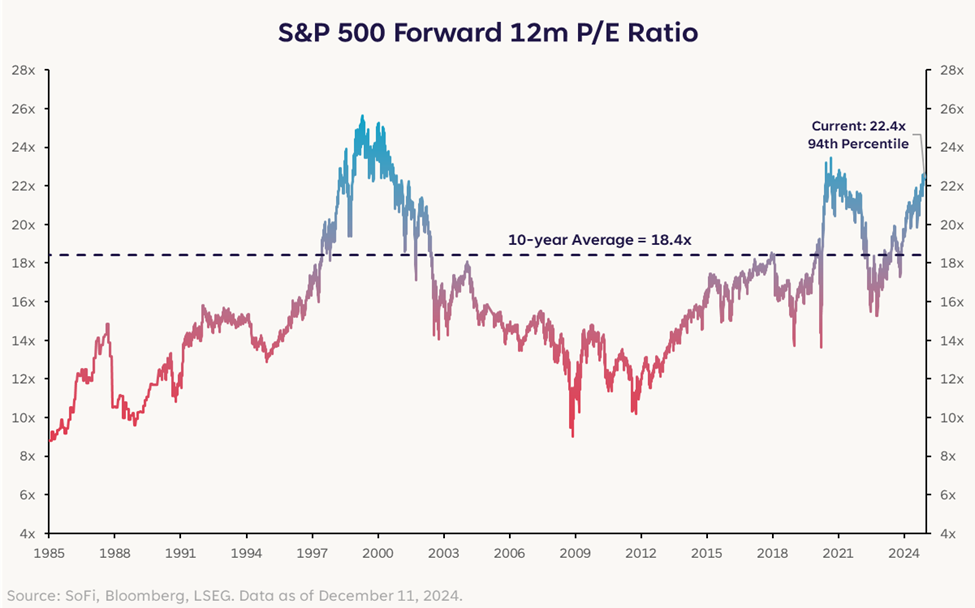

But what about valuations? They’re high compared to history, that’s a simple fact. The S&P 500 is currently trading at 22.4x forward earnings, compared to the 10-year average of 18.4x.

Interestingly though, the average annual return on the S&P 500 is nearly 12%, and if earnings growth comes in over 14%, as expected, an average return on the S&P could actually result in a stable or lower price-to-earnings multiple before the end of the year, keeping bubble fears at bay.

In many ways, the fact that most investors do not expect another >25% year in the S&P is a good thing. If we were to produce a third year of rip-roaring returns, valuations would look even more stretched – if not exuberant – and likely drive volatility as investors try to manage exposures. An “average” year of returns may be what this market needs to stay rational.

What it all means for Yields

There’s been endless speculation on how high (or how low) Treasury yields will go. We don’t expect that to end in 2025. What we do expect though, is for yields to gradually come down as long as inflation stays contained.

A gradual drop in yields can be supportive of equities and sentiment, but contrary to expectations at the beginning of 2024, the Fed is unlikely to cut rates dramatically unless the economy weakens in a material way. This means markets and the economy may need to get (or stay) comfortable with a neutral rate that’s above pre-pandemic levels, and a 10-year Treasury yield that’s elevated as well.

Where Things Could Go Wrong

As with any new year comes new risks, or at least extensions of the prior year’s risks. To repeat a point from the beginning of this piece, we can’t invest by waiting for historical precedent to repeat. We do, however, have to keep in mind the risks we know exist as we allocate portfolios with the fresh eyes of January.

Risk #1: Sentiment Becomes Overdone, Speculation Overheats

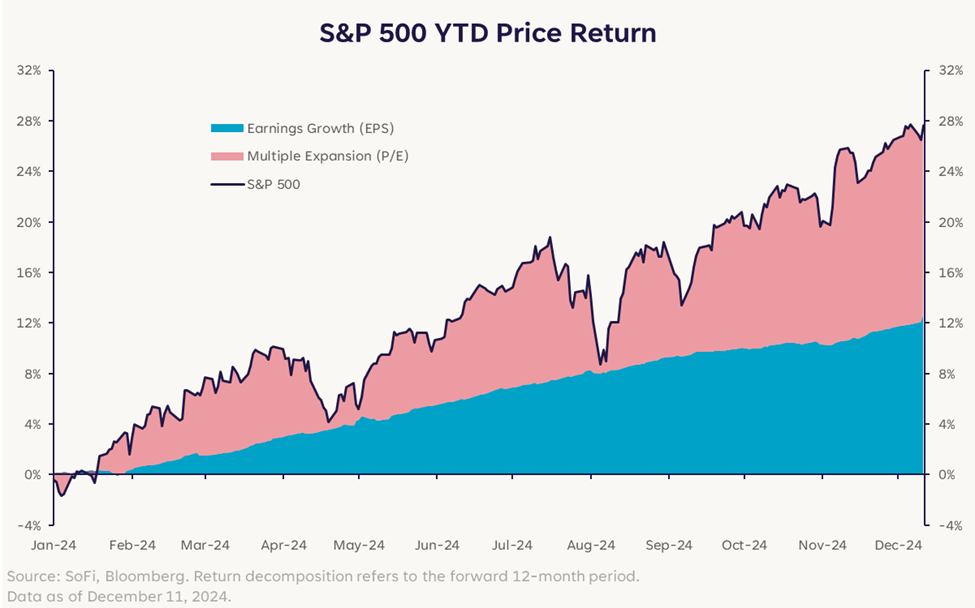

We currently view the positive sentiment as a tailwind for markets that can continue into the first half of 2025, but there is a risk that sentiment could become over-extended and drive excess speculation in the financial system. There’s no hard-and-fast measure that can declare when we’re overheated, but something we like to track is the proportion of stock returns driven by earnings growth (i.e. fundamentals) versus multiple expansion (i.e. sentiment-driven upside).

The reason we track this is because the more of a rally that can be attributed to multiple expansion, the more fragile that rally can be. Some sentiment-driven upside is good as markets anticipate brighter days ahead, but it can turn into a chase as investors become greedy and start blindly buying risk assets.

The recent rally shows an increase in multiple expansion as a driver, but we could also argue that the business environment may change for the better in 2025 and might deserve the resulting upside.

Another way to look for excess speculation is through the lens of high quality vs. low quality asset performance. As investors increasingly pile into lower quality — therefore riskier — investments, speculation rises. One specific example of this is between mega-cap tech stocks versus those of non-profitable tech companies.

The recent outperformance of non-profitable tech stocks suggests investors have amped up their risk appetite, which is not a red flag in and of itself. Increased risk appetite could be warranted given some possible changes in the business environment in 2025 — but it’s a speculative move, nevertheless.

Lastly, much of the recent bump in sentiment has been predicated on the expectation of policies from the incoming administration that would reduce regulations, reign in government spending, and encourage stronger economic growth. Asset classes that have benefited from those expectations so far are financials, consumer discretionary, small-cap stocks, and crypto. On the flipside, there are some groups that have been hurt by new policy expectations such as health care, gold, and international stocks.

The concern is that if the expected policies do not come to fruition, or if they end up being different or less powerful than the market has priced itself for, we could see an unwind of the positive sentiment in some groups and a repricing in those that have been hit.

Expect policy volatility to continue in the first half.

Risk #2: Inflation Reignites => Fed Turns Hawkish => Yields Spike

It seems like a lot has to happen for this risk to materialize, but it could prove to be more possible than markets are appreciating. Inflation measures have come down considerably, but they’re currently stuck at levels above the Fed’s target.

If 2025 turns out to be one of stronger-than-expected consumer spending, and stronger-than-expected business investment, the resulting demand could again push prices higher. Moreover, if that’s happening with the backdrop of increasing tariffs and a reduction in the workforce due to lower immigration, costs could be driven up across multiple industries.

The possible reduction in supply and increased domestic demand could push inflation upward, and in turn pressure the Fed to stop cutting rates.

Yields are another aspect of this risk that can’t be ignored. Reheating inflation and a hawkish Fed could drive them higher, as well as the possibility of government spending remaining high while the budget deficit continues to grow. If the Treasury increases its issuance of debt, the market would need to find buyers to absorb that debt, thus pushing yields up further. The TGA can support us for a while, but not forever.

Risk #3: AI Fails to Be Monetized, Earnings Disappoint

This last risk we point out is more likely to be relevant for right now, but not forever. Eventually, we do expect AI to prove successful in various industries, but the theme is still in its infancy and it’s impossible to know how it may morph in the years to come.

Investors have already grown a bit impatient as it pertains to proof of profit for companies that have spent large amounts of CapEx on AI initiatives. In 2025, that scrutiny is likely to stick around and even increase. If companies are able to show real financial benefit, productivity, and innovation gains as a result of their AI-related spending, this risk dissipates. But if tangible results remain elusive, continued stellar earnings growth and stock price upside could also become elusive.

What Catches Our Eye in 2025

With this as a backdrop, here are a few areas we believe have tailwinds in 2025.

- Software

- May be poised for a catch-up trade versus semiconductors as investors search for new pockets of growth with a lower hurdle rate.

- Could benefit from increased business capital expenditure in 2025.

- We believe this could be a next-phase beneficiary of the AI theme — a conduit for how the concepts can be brought to life.

- Gold

- Institutional and international central bank appetite for gold is still strong, and it could further benefit from an increase in retail investor participation.

- Global political uncertainty is likely here to stay, gold is typically a beneficiary of policy and currency volatility around the world.

- Cyclical Sectors: Financials, Industrials, Energy, Materials

- These may not produce the tech-like returns of 2023 and 2024, but a pro-growth environment with looser regulations could make 2025 a friendly cyclical environment.

- These may not produce the tech-like returns of 2023 and 2024, but a pro-growth environment with looser regulations could make 2025 a friendly cyclical environment.

- Health Care

- A contrarian pick, as we believe much of the bad news and risks are already priced in. Any improvement in sentiment could drive a repricing upward.

- Expected to produce strong earnings growth in 2025, bested only by technology.

- China

- Another contrarian pick given the incoming administration’s well-telegraphed plans to limit China’s trade with the U.S., but we also believe much of the bad news is already priced in.

- China’s sluggish growth may drive the country to announce more stimulus in 2025, and present an opportunity for upside.

Of course, if any of the above mentioned risks come to fruition, or other negative surprises occur, these investment implications would change. But absent a change in the investing or macro environment, we find these pockets of the market to be compelling.

Conclusion

The end of one year and beginning of the next is always a time for reflection and re-positioning. We believe 2025 has the potential to be a positive year for markets and the economy, albeit more muted than the past two years, and with its own set of risks and uncertainties.

This cycle’s economic and market resilience has been remarkable and is one for the history books. Looking back, in many ways it has been warranted. After all, the market is never wrong — it’s simply a reflection of investor sentiment and the outlook for growth prospects down the road. We choose optimism into 2025 and look forward to the new opportunities and surprises it will bring.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, investment advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.