Looking at: The Return of Small-Caps

Estimated reading time: 5 minutes

Peanut Gallery

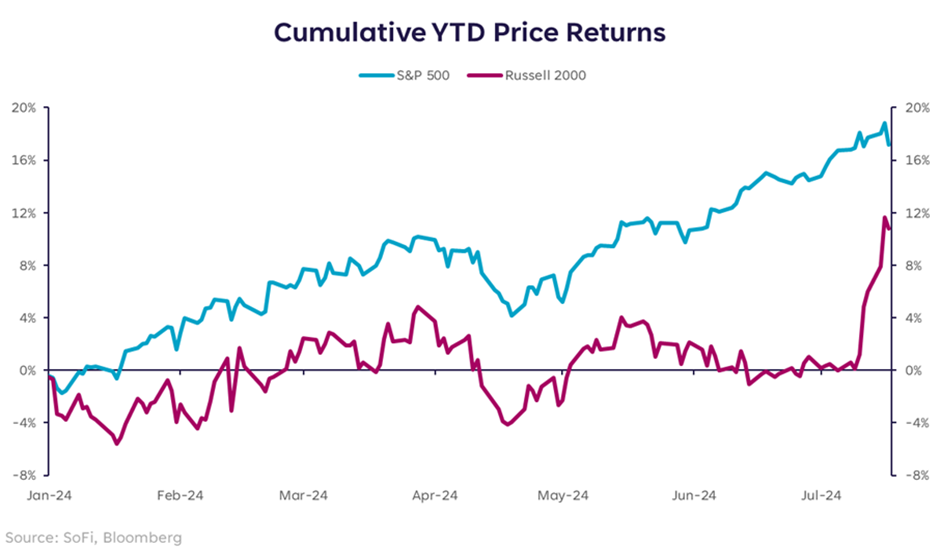

In case you missed it, small-cap stocks have staged quite the rally of late. In just over one week, the Russell 2000 rose over 10%. To put that in perspective, the small-cap index had a move so large that it accomplished in seven trading days what many investors were hoping it would for the last two and a half years.

Not to mention, before this move, the S&P 500 was outperforming the Russell 2000 by 16% year-to-date; now that gap has narrowed to just 6%.

As a long-time supporter of small-caps, I love to see this. But at the same time, a move this dramatic in any asset class or security can leave us wondering: Can it last? After all, small-caps have attempted a comeback multiple times throughout this market cycle (five, to be exact) and failed to reach new highs despite large-cap indices continuing to outdo themselves.

Breaking Out of Their Shell

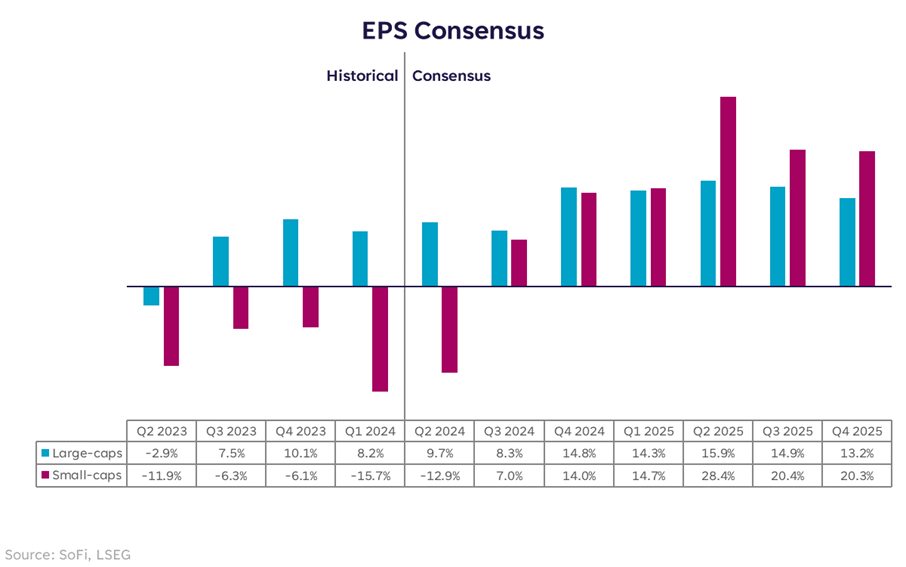

In this environment where much of the commentary has turned back to fundamentals — topics such as earnings growth, quality of the balance sheet, and competitive strength — one place we can look to analyze the staying power of small-caps is their quarterly results.

The chart below compares quarterly earnings growth of the S&P 500 to that of the Russell 2000. It’s clear that large-cap earnings have outpaced small-cap earnings over the past year, and knowing how strong the results have been for big tech companies, this is no surprise.

What’s more compelling is the trend of future projections. Consensus expectations are for small-caps to see a strong resurgence in earnings growth starting in Q3 of this year. If that’s the case, and if markets are forward looking mechanisms, a surge in small-caps could be warranted given that earnings are expected to handily outpace large-caps by the end of next year.

The fundamental story appears to be in place, but what about the environmental story?

Nuts About Cuts

Here’s the curious piece — we already knew what the earnings projections were before this recent two week run, but small-caps were flat for the year. The sudden move cannot be entirely based on future earnings growth, that’s not new information.

The new information has been a combination of lower U.S. Treasury yields, cooler inflation data, and increased risk appetite on the possibility of a more certain U.S. election outcome. The earnings data helps to confirm that the move has fundamental support from the index, but likely wasn’t the driving force.

Since the beginning of July, 10-year Treasury yields have fallen from 4.46% to 4.15%; likewise, 2-year yields have fallen from 4.76% to 4.43%. A change of nearly 30 basis points in the two most indicative points on the yield curve are major market moves… especially in such a short amount of time.

Small-cap stocks are more rate sensitive than large-caps because they tend to carry more leverage and are more likely to be financed with floating rate debt. As such, a move down in rates can have more dramatic effects on small-cap sentiment.

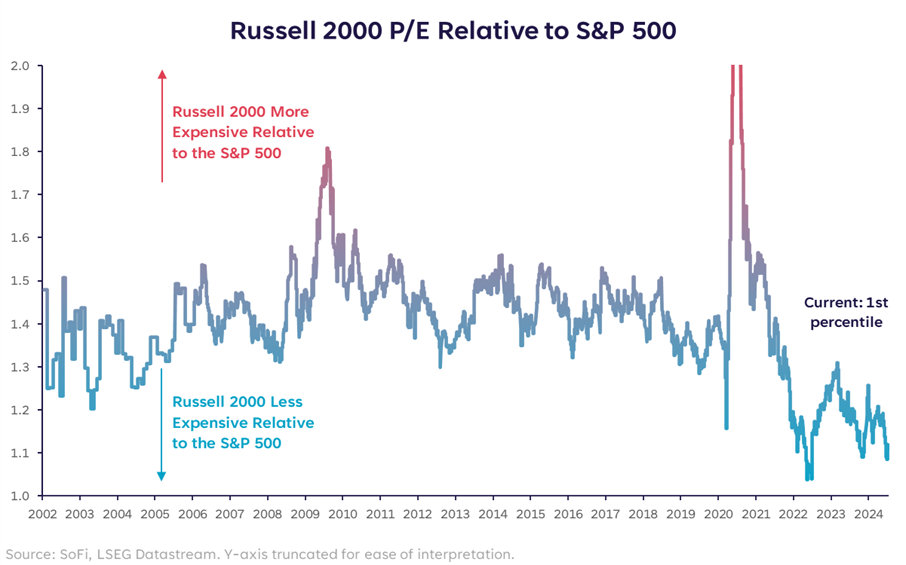

The last part of this discussion is valuations: Even with a recent rally, small-caps are attractively valued relative to history. To be clear, the forward P/E on the Russell 2000 is higher than that of the S&P, but it usually is because of the typically smaller earnings (the “E” in P/E) in small-caps, but the current ratio between the two indices is so low that it’s only in the 1st percentile.

Part of that is due to the fact that large-cap valuations are currently quite high and sitting in the 92nd percentile, but if we’re looking at this on a purely relative basis, small-caps appear to be trading at an attractive price point.

The caution I’d provide is this: As the Fed embarks on a rate cutting cycle, markets tend to cheer it initially and even for a short period after the cuts begin. But if that cutting cycle occurs in concert with slowing economic data, disappointing earnings, or a quick compression in multiples, small-caps would likely lose steam quickly.

Not to mention, the Fed typically cuts rates late in the economic cycle, not early in the cycle when small-caps tend to have their moment in the spotlight.

In the near-term, this rotation into smalls can continue. Markets are looking forward to easier monetary conditions, and they’re likely to get them this fall. The question is whether that will be followed by a slow and steady cooling in inflation and jobs, or a quick and painful one.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, investment advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.