Looking at: The Latest Inflation Numbers

Estimated reading time: 0 minutes

Demoted

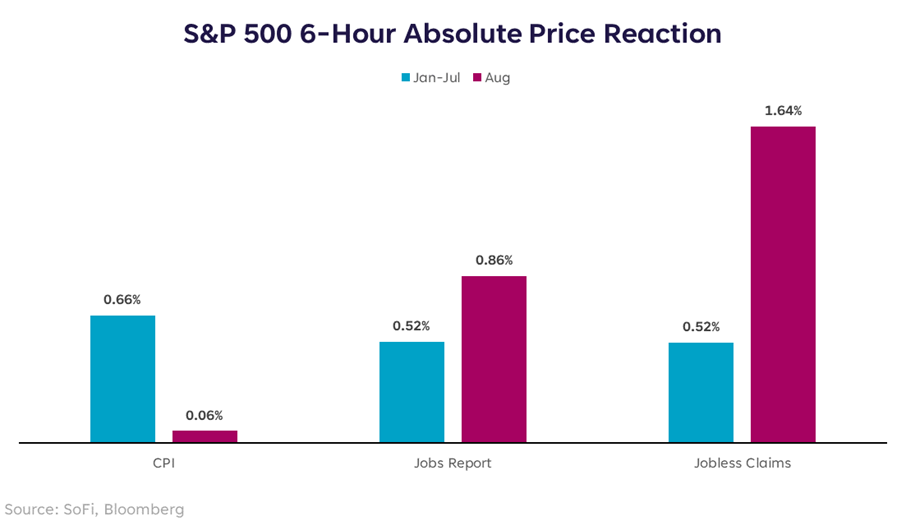

Inflation data has been demoted to second-most important economic data, having been recently surpassed by jobs data.

We can not only hear this in the commentary around markets, but also in the market reactions of late. The one-day reactions in the S&P 500 have become more muted for inflation releases and more pronounced for labor market releases. Investors are now more focused on employment, and for good reason… it seems to be the key to predicting what the Federal Reserve might do with rates for the rest of the year.

But have we slayed the inflation dragon? What about all the fears of a resurgence in prices if the Fed cuts too soon, or if input costs rise again, or if shelter and car insurance just never ever ever come back down?

Expectations Feed Demand

Still those are valid concerns, and a resurgence is a possibility, especially in the case of a shock to energy prices or to commodities that affect raw materials prices. Those are typically caused by events outside our control that are unpredictable. It’s safe to say exogenous shocks are always a risk, and until or unless they become more obvious or imminent, there’s little value in trying to invest “around” them.

Outside of an exogenous shock, what else might cause inflation to heat back up? Growth surprising to the upside, which likely means demand has picked up and is again outstripping supply. A renewed economic overheating, so to speak. That’s the scenario the Fed believes they have more control over, and is the exact outcome they’re trying to avoid. Hence the long pause before beginning to cut rates.

In my opinion, the risk of that is the lowest it’s been in this entire cycle. There’s been a tone shift, and the most recent jobs report that came in weaker than expectations drove that home. I’ve long said consumers will continue spending as long as they feel confident in the employment picture, and I believe that confidence has been shaken.

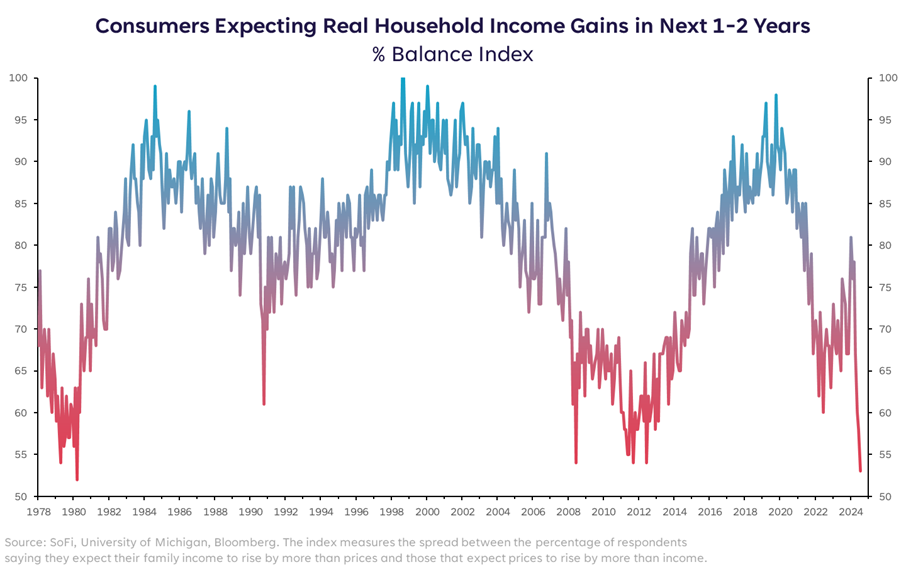

One of the ways we can measure this is using the Conference Board survey of consumer confidence. We’ve stripped out a couple relevant components in the chart below, and can see a sharp decline in consumer expectations of real household income.

If consumers increasingly believe their real household income will be lower in the future than it is today, they’re not likely to increase their spending. Moreover, a rate cut isn’t likely to change their minds very easily. Which also means, I believe it’s time to start cutting.

Proof is in the Guidance

Q2 earnings season has been solid, posting a 12% year-over-year growth rate so far (91% of S&P 500 companies have reported), which is above the original expectation of 8.5%. But as we know, it’s just as much about how companies did last quarter as it is about what management expects in future quarters.

There’s been a general theme of guiding down, with a number of bellwether consumer companies in leisure and hospitality (e.g. Marriott, Hilton, Norwegian), restaurants (e.g. McDonalds, Starbucks), and others (e.g. Home Depot, LVMH, Visa) either already seeing a slowdown in customer demand or expecting some sort of pullback in consumer spending for Q3 and Q4.

To be clear, we needed a pullback in spending in order to cool inflation and keep it on a sustainable path toward the Fed’s target. We also needed a reduction in the risk that demand would heat back up if we cut too soon. I believe both are currently the case, and markets seem to as well. So despite the fact that this week’s big headline data was the consumer price index, we remain more focused on the labor market as the more important clue.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, investment advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.