Looking at: The Fed’s July Statement

Estimated reading time: 5 minutes

The Case for September

Rates remained unchanged, and the expectation for the Fed’s first rate cut to occur in September remained in place. Much of Jerome Powell’s commentary this year has centered around wanting “more confidence” that inflation was moving sustainably toward the Fed’s 2% target. Today, he stated that data from the second quarter added to their confidence, though they still need more.

Other comments from Powell today indicated that the data suggest the economy is moving closer to a state where it would be appropriate for them to cut rates. Of course, the data between now and September will be the main decision factor of whether or not cuts actually begin.

Markets loved it. Stocks were already rallying before the meeting and found a further tailwind from Powell’s comments. Treasurys also rallied, with the short-term yields coming down further than long-term yields, suggesting that a cutting cycle is more assured. Investors still view cuts as bullish for assets, and they may be… initially.

Room to Respond

Despite the market clamoring for cuts, the Fed maintains a view that the case for cuts is not yet clear. They continue to weigh the risks of moving too soon against the risks of moving too late. There’s a belief that the Fed is typically late to move rates, both on the upside and the downside. The question now is: Will waiting until September be too long? Said another way, will they have kept policy restrictive longer than necessary?

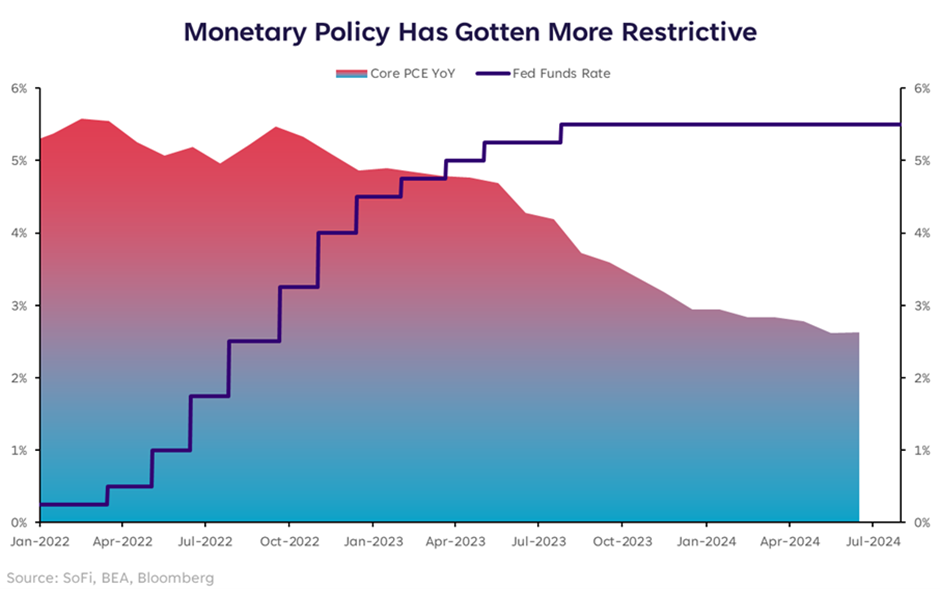

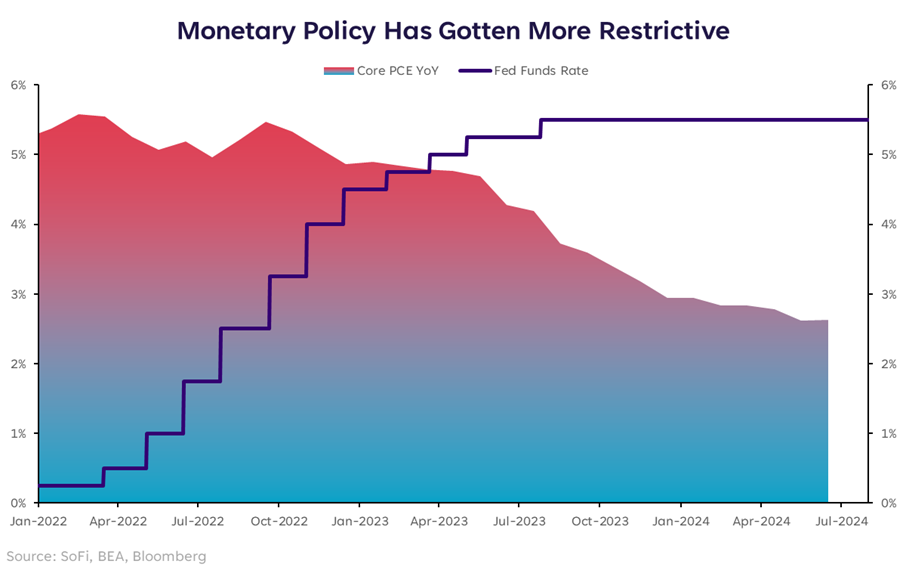

The chart below shows a measure of “restrictive policy” with the fed funds rate above the Fed’s preferred inflation measure since March 2023.

There is no magic number of months that policy should remain restrictive, but if labor market conditions weaken considerably between now and September 18th, it will appear that they waited too long. In that scenario, markets are likely to get jittery.

The risk now in my eyes is that if they start cutting after economic data has weakened, those cuts will start to look like a panicky response to a troubled economy rather than a gentle normalization of policy. Labor market data is what has the power to shift that perspective, in my opinion.

But with a Fed Funds rate upper bound at 5.5%, they have a lot of room to respond to any surprisingly weak economic data, which provides a decent buffer.

Jobs Teeter Totter

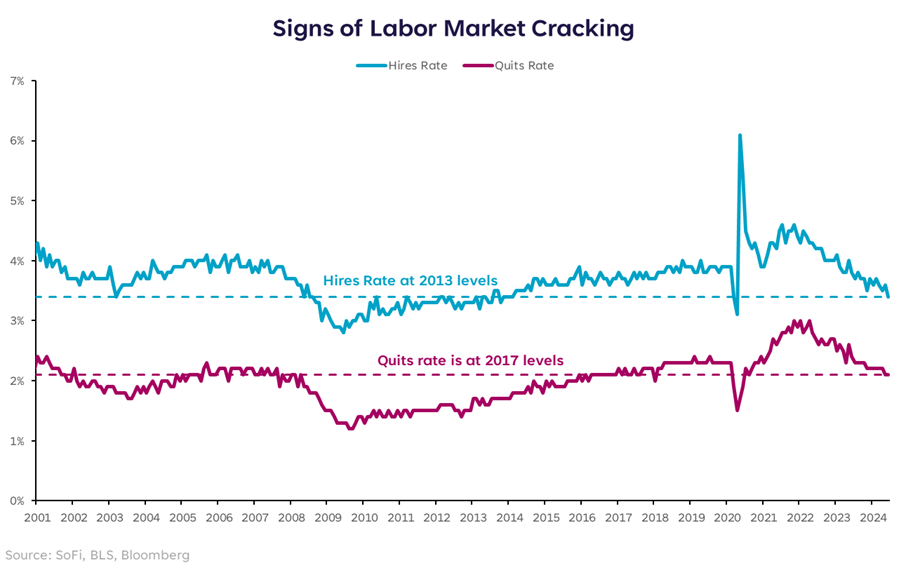

If labor data hold the key, there are a few recent signs that warrant watching. In my view, the labor market has cooled to a point of being in a sweet spot, but if it cools much more it will tip over into a concerning spot.

As it stands now, the demand for workers and the number of workers available is in good balance. The employment cost index has come down to a more palatable level. Layoffs have not picked up meaningfully, and the unemployment rate is higher than it was a year ago, but still comfortably low at 4.1%.

A couple pieces of data that have moved down notably are the hires rate and the quits rate. Basically, the pace at which employers are hiring and the pace at which workers are voluntarily quitting. Both show consistent slowing that indicates the labor market has cooled to levels not seen since long before the pandemic. We don’t want to see these go down too much further.

The July jobs data comes out this Friday, and it will be important to watch. We’ll also have August’s jobs data before the Fed’s next meeting in September. As Jerome Powell constantly reinforces, it’s never about one particular data point, it’s about the totality of the data. But I believe the most important data to pay attention to for signs of economic health and thus, possible Fed moves, are all things labor related.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, investment advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.