Looking at: Market Whiplash

Estimated reading time: 5 minutes

Up, Down, and All Around

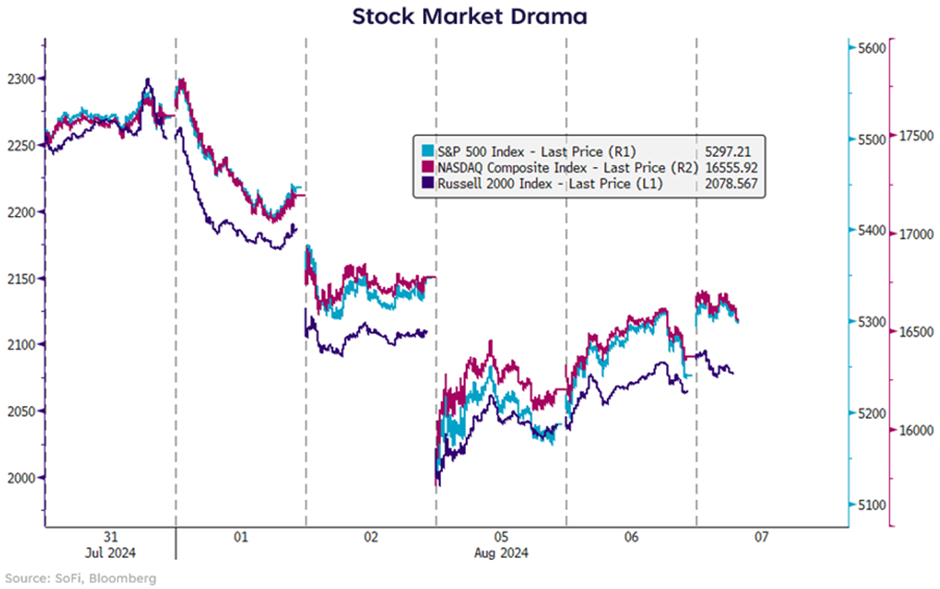

What a week. A seemingly minor pullback began last Thursday after some weaker-than-expected U.S. manufacturing data, which was exacerbated by a weaker-than-expected Jobs report on Friday, and then the whammy of major stock market volatility in Japan over the weekend sent the S&P volatility index (VIX) to 65 on Monday and the S&P 500 index down 3% in one day.

But then, things bounced back. The VIX is back down in the low 20s, the S&P has risen 2.5% since Monday’s close, and the Nasdaq is up 2.8%. Treasury yields have completely erased their dramatic drop during the height of fear on Monday, and despite the 2s/10s yield curve inversion briefly turning positive, it’s squarely back in negative territory.

Talk about whiplash. Investors are still on edge, not sure whether to trust this new rally, and wondering if the Fed will do anything differently as a result of the drama.

Pullbacks are Not Emergencies

In the hysteria of Monday’s volatility, there was chatter about whether the Fed should perform an emergency inter-meeting rate cut in response to the pullback. Some market participants were feeling impatient and viewed the expected September rate cut as too far away.

But pullbacks are not emergencies. Volatility is not an emergency. Stocks falling from a P/E of 21.1x down to 19.8x is not an emergency. In my opinion, the only market-related circumstances that would call for an emergency rate cut are severe dislocations that prevent the market from functioning properly, thus threatening the stability of the financial system. These would be things such as triggering index-wide circuit breakers in the U.S., a seizing up of liquidity in bond markets, extreme and nonsensical moves in commodity contracts, or a large publicly traded company blowing up that has a high probability of contagion.

Other non-market circumstances that could warrant an emergency rate cut would be geopolitical crises, broad-reaching natural disasters, wars, global health crises, or other black swan events.

None of those things are what drove this volatility, or at least not in an extreme enough manner to require an inter-meeting rate cut, which would only breed further panic, in my view.

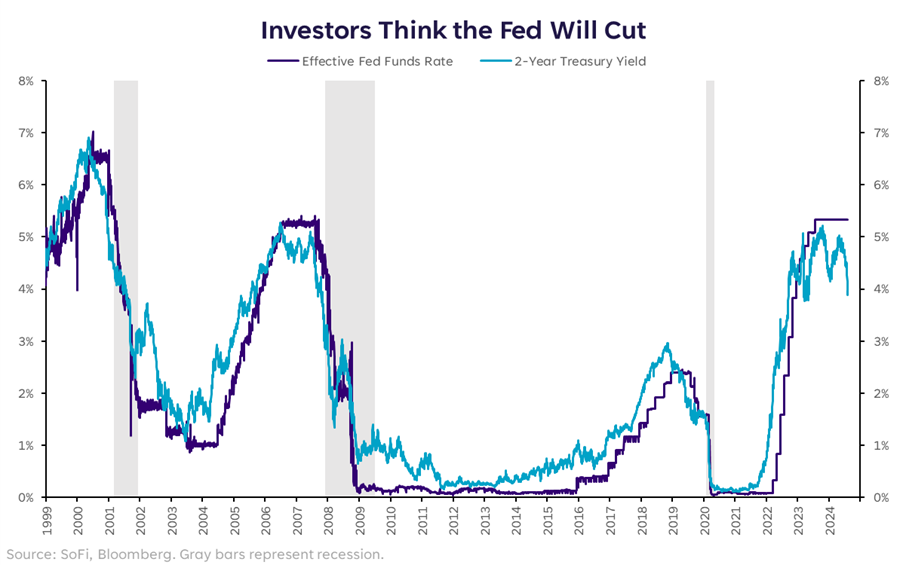

That said, the market is still asking for rate cuts and using the 2-year Treasury yield as its messaging platform. The chart below shows the current spread between the effective fed funds rate and the 2-year Treasury yield, which generally track each other tightly, except in times of rate volatility.

The difference between the two is currently 1.31% or 131 basis points, with the 2-year much lower than the fed funds rate, meaning investors are expecting (hoping) for rate cuts in the near-term.

To put it in perspective, the last time the spread was this wide was in October 2008. And this large of a spread is in the third percentile of all readings since 1976. The environment in 2008 was wrought with long-lasting spells of volatility, different from what we just experienced, so it would be unfair to draw direct comparisons. But it’s at least safe to say things are currently measuring on an extreme end of the spectrum compared to history.

But why does it matter for markets? Because when the market believes yields are going lower in a jiffy, it has historically been a pre-recession warning. That doesn’t mean it will be this time, but at the very least it shows us that markets have backpedaled on the soft landing narrative and started baking in an increased possibility of a hard landing.

On the Edge

Even if that nerve racking event is over, we learned how sensitive markets now are to cooler U.S. economic data, how broad reaching the impact of the Yen carry trade can be, and how conditioned investors are to expect rate cuts as the salve for every scrape.

This is a different market environment from mere months ago, and one that is more balanced in its assessment of risk. Unfortunately, that means it’s also less certain about the future path of the economy, but to me this feels like a more rational view of the possibilities.

We believe there is more volatility to come, and cooler economic and earnings data that will need to be digested for the remainder of the year. If we needed a reminder of why portfolios should remain diversified, even during periods of concentrated rallies, we just got it. Volatility can be unsettling, but it can also be an opportunity to revisit your allocations and do a gut check on what level of risk you’re comfortable with, given the wide variety of possible outcomes.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, investment advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.