Investment Strategy View: Macro Pulse

Estimated reading time: 0 minutes

Cruising Altitude

Remember in 2022 when Federal Reserve Chair Jerome Powell warned that getting the economy back into balance would involve some economic pain? The road since has been long and winding, but two years later we’ve managed to avoid a recession (knock on wood). While interest rates rose significantly, hard landing fears never became reality, and the economy found a bit of a sweet spot. That’s a big reason why stocks have been able to rise nearly 70% since their cycle bottom in October 2022.

With just one month left to go in this whirlwind of a year, it might be a good idea to catch our breath and evaluate the state of play.

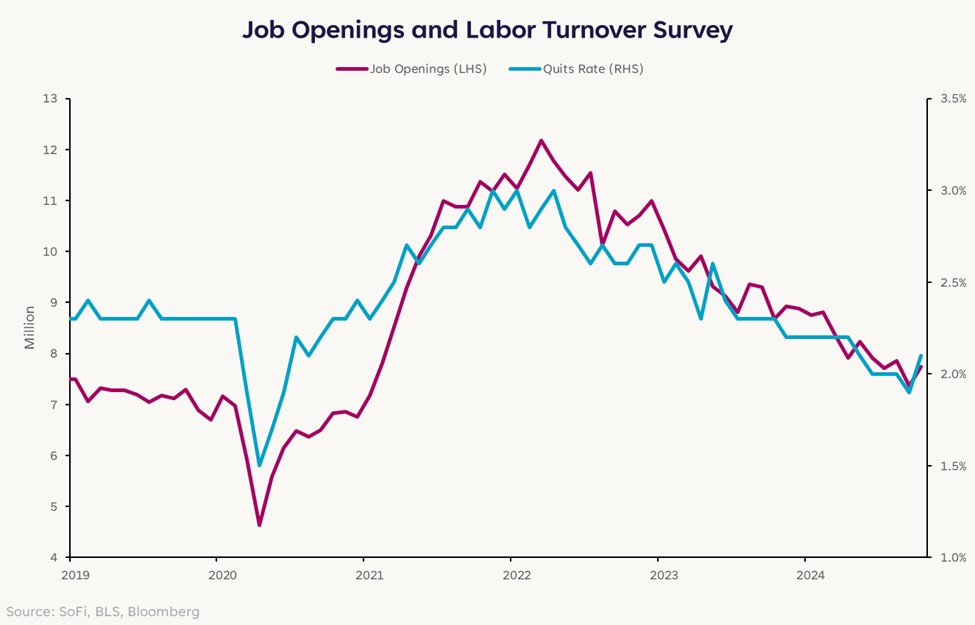

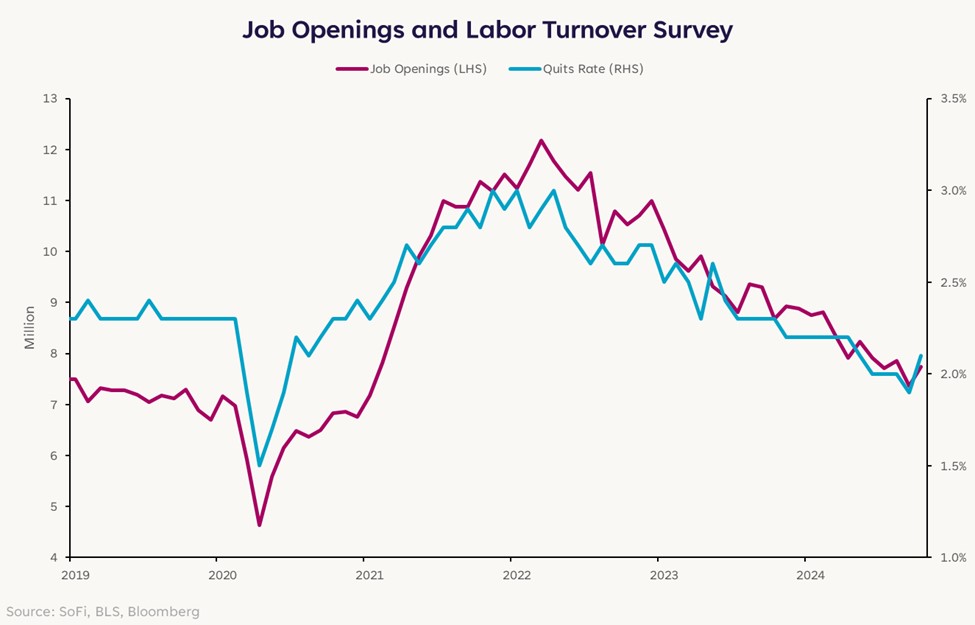

Labor Bedrock

The main driver of the U.S. economy is consumer spending, with the labor market as the backbone. More jobs drives more income, more income drives spending, more spending drives economic growth – so the story goes. While the monthly jobs report is probably the single best data point we can use to judge how the labor market is doing, this note will be published before we get the report for November. Still, there are other indicators we can use to get a feel for the employment backdrop.

We already got some data this week in the form of the Job Openings and Labor Turnover Survey (JOLTS). JOLTS showed an increase in job openings and quits rates, breaking a recent downward trend, though hiring rates remained low.

On the other hand, there are some conflicting signals. For instance, initial jobless claims have been falling (suggesting labor strengthening), yet continuing claims are at their highest levels in three years (suggesting labor weakness). Additionally, we also got ISM Purchasing Managers’ Indexes (PMIs), which showed nuanced differences between sectors. The manufacturing survey showed employment improvement while the services survey showed cooling. But really, what the data shows more than anything is low labor churn and a market that has simply stabilized.

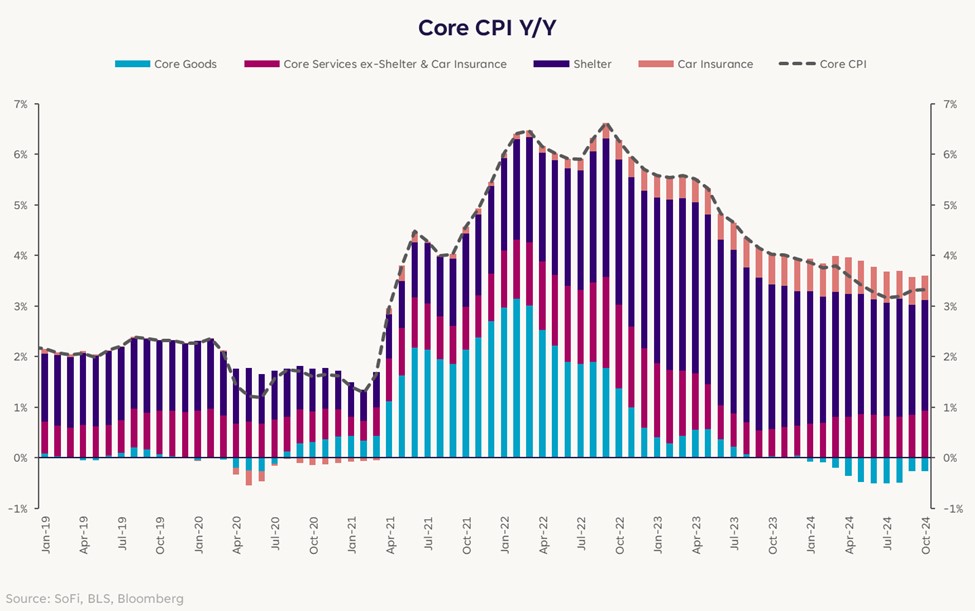

Price Pressure Valve

Inflation remains a focal point of analysis for investors and the Fed. The current trajectory still shows gradual moderation, though the process has been slower than some anticipated and has even stalled of late. The main reasons for the stickiness are slow-moving components like shelter and auto insurance, which are keeping the broader inflation measures above target.

Just like the PMIs gave conflicting signals on the employment front, the surveys’ price signals are also muddied. The manufacturing survey showed a downside surprise to price pressures, while the services survey showed input costs were more sticky than expected. Given that Fed officials are debating whether to slow the pace of interest rate cuts, conflicting inflation signals could push them to lean on the side of caution and end the cutting cycle earlier than expected. That would put a floor beneath Treasury yields and could drive some upside yield volatility in the meantime.

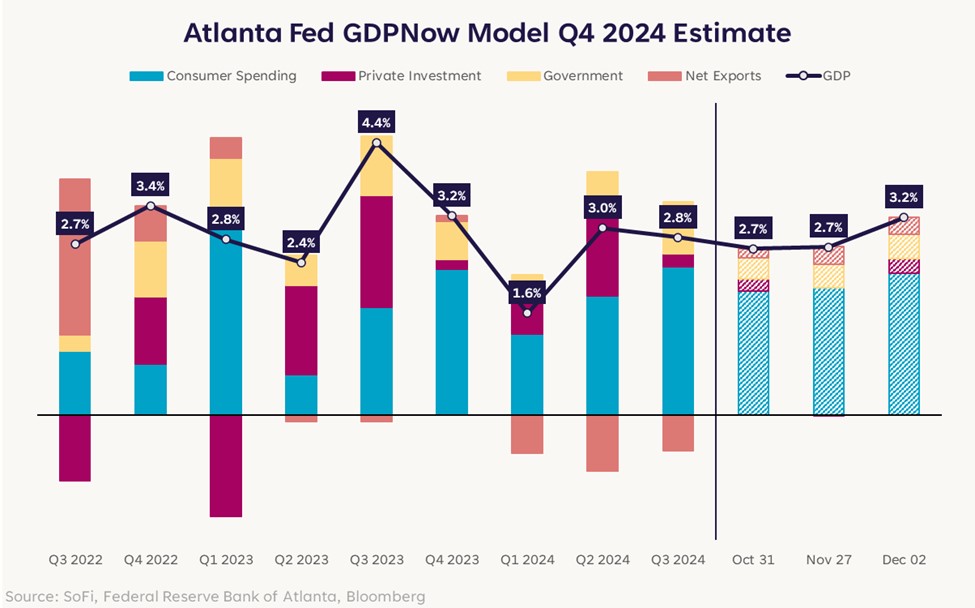

Smooth Sailing

Most data points to strong growth momentum: Consumer confidence is improving, the new orders components for both manufacturing and services PMIs remain in positive territory, and vehicle sales surprised to the upside. Even looking back on the recent earnings season, earnings growth came in nearly 8% above consensus estimates. It should come as no surprise then that GDP growth is tracking toward another above-trend quarter, which would make it the eighth such quarter in the last nine.

As such, stocks have been able to do well and Treasury yields have remained elevated given these resilient economic fundamentals. And given how stable the macro backdrop has been, betting on a big shift in market dynamics right now might not be the right move. The upward momentum status quo could be with us for a while longer. Stay vigilant.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, investment advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.