Decoding Markets: Rebalancing Act

Estimated reading time: 6 minutes

History as a Guide

With just a few days left in the first quarter, the euphoria investors generally felt coming into the year has been zapped. The S&P 500 briefly fell into correction territory on March 13, dropping 10% from its recent peak before rebounding a bit.That has rattled some investors, who may have grown accustomed to the robust returns of 2023 and 2024, when the index rose 24.2% and 23.3%, respectively.

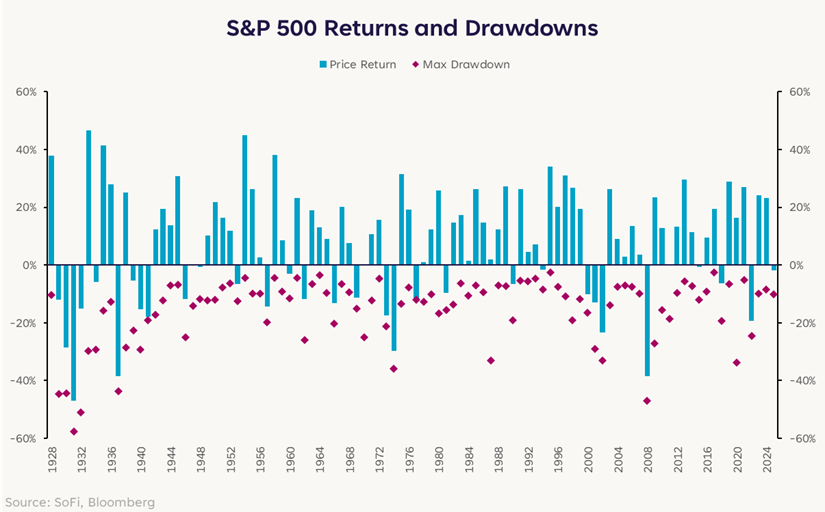

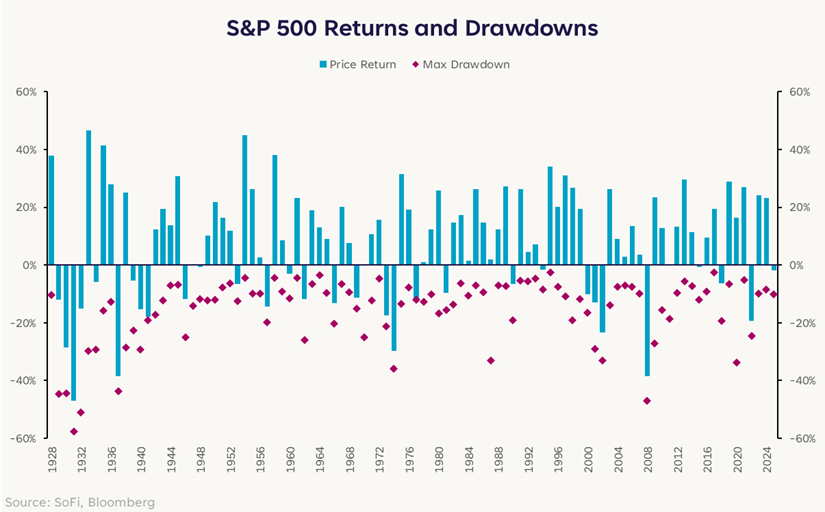

This pullback was actually not that shocking when viewed through a historical lens. Since 1946, the S&P 500 has experienced an average intra-year decline of 13%, with the market seeing a double-digit percentage drawdown over half the time. Against those stats, this year’s drawdown might even appear mild, the speed of the decline notwithstanding.

The thing for long-term investors to focus on is that despite the tendency for significant intra-year declines, stocks frequently recover to end the year in positive territory. It can be dangerous to overreact to short-term volatility, as market timing attempts frequently lead to missed rebounds. What has happened in the last two weeks is a case in point: The S&P 500 is up 4% since March 13, though it’s still down 2% on the year so far.

A Relative Underperformance Story

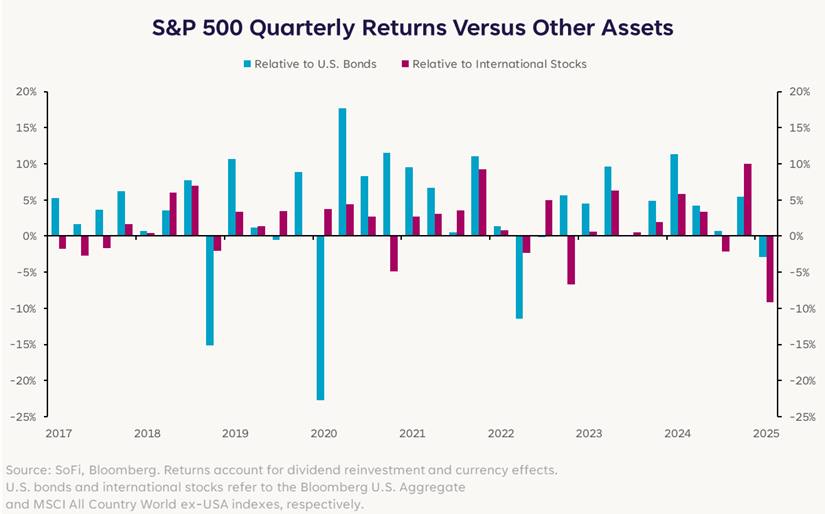

What makes the current market dynamic particularly interesting is the relative performance story. Despite the tough sledding for U.S. stocks, Europe’s Euro Stoxx 50 index has had a total return (accounting for dividends and currency appreciation) of +17.1% in Q1 alone. If the year ended today, that would be the fourth-best year of performance in the last 12 years and well above the annual average of +10.1%. That means that European stocks outperformed U.S. stocks by 18.0 percentage points this quarter. If that number holds over the next few days, it would be the single-largest quarterly divergence since data became available in 1992.

Broader international markets are having their best quarter versus the S&P 500 since Q2 2009, while U.S. bonds are beating domestic stocks for the first time in nearly three years. Since we’re coming up on the end of the quarter, the possibility of big portfolio rebalancing moves looms large given the divergence. For the uninitiated, large institutional investors such as retirement funds, endowments, and foundations generally have strategic asset allocation levels that they need to closely stick to. If a position moves too far away from the target level – whether due to market volatility or a long stretch of outperformance – the portfolio is usually rebalanced to bring things back to acceptable levels.

Considering the U.S. stock market’s long stretch of outperformance and the suddenness of the reversal, it’s possible this quarter-end period is more eventful than usual. Rebalancing is effectively a mean reversion trade: The stuff that has done best is sold (to bring their allocation down to the target), while the stuff that has lagged is bought (to bring their allocation up to the target).

In today’s market environment, that could mean temporary buying support for U.S. equities that have fallen below target weights. Conversely, some profit-taking could emerge in international stocks that may have grown oversized. While these flows can influence short-term market movements, they don’t necessarily signal a fundamental shift in sentiment or economic outlook.

Valuation Gaps

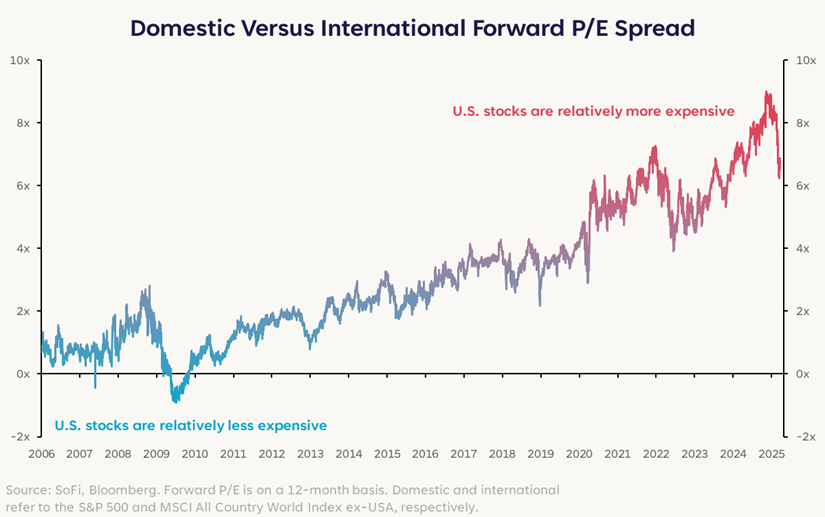

Valuations are one of the main ways investor sentiment manifests itself. Investor willingness to pay more for the same earnings suggests optimism, and vice versa. For investors bullish on international markets coming into the year, a common refrain was that relatively attractive valuations meant that there was room for multiple expansion if sentiment improved. Additionally, lower starting multiples could provide a potential buffer against market volatility, since there would be less room for sentiment to worsen and cause multiples to decline further.

At the end of 2024, the S&P 500 had a forward 12-month P/E ratio of 21.6x, while the rest of the world had a multiple of 13.4x. While some valuation differential makes sense due to different sector composition – the United States has most of the large, high-growth technology companies – the spread between the two ranked in the 98th percentile.

The gap has narrowed noticeably in 2025, but it remains elevated. Considering the potential for major upheaval to economic policy and global trade, elevated market volatility could be with us for the foreseeable future. The longer-term story is complicated (no surprise there). Quarter-end rebalancing flows could boost U.S. stocks in the short-term, but higher valuations represent a risk if sentiment takes another turn lower. The longer-term story is as complicated as ever, reinforcing the need to diversify portfolios not only across sectors, but regions too.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, investment advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.