Hot January Inflation

Estimated reading time: 6 minutes

Drop Because It’s Hot

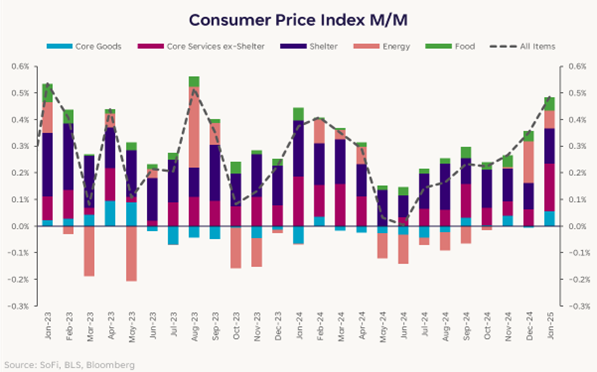

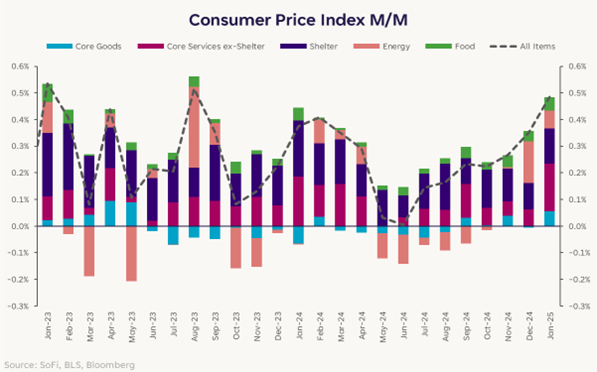

The first Consumer Price Index (CPI) data of 2025 is in and it was hotter than expected across the board. Headline CPI (the index including all items) came in at 0.5% m/m and 3.0% y/y versus estimates of 0.3% and 2.9%, respectively. Core CPI (which excludes food and energy) wasn’t much better, coming in at 0.4% m/m and 3.3% y/y versus estimates of 0.3% and 3.1%, respectively.

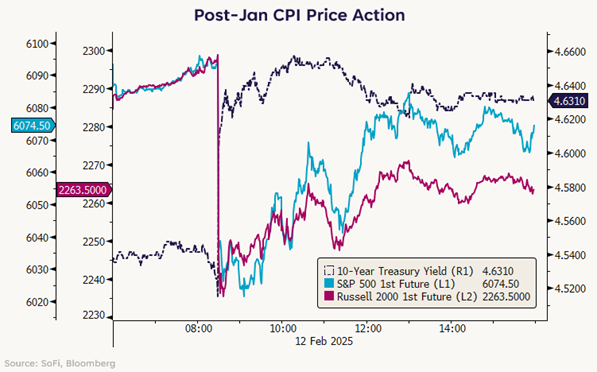

No surprise that markets reacted poorly, with 10-year Treasury yields rising by 15 basis points (bps) and 2-year yields rising by 9 bps. Concurrently, the market’s expectation of Fed interest rate cuts fell to just one cut in all of 2025, and pushed the following cut out to the second half of 2026.

While stocks fell immediately following the report, they clawed much of those losses back by the end of the day. Treasury yields, however, held relatively steady at a much higher level than when the day began. The message this sends is that problematic inflation leaves very few places to hide, though investors are still inclined to shrug off fears in the near-term.

Built to Last?

As with most knee-jerk market reactions, this could be erased quite quickly if investors decide this report is more of a blip than a sign of a lasting problem. Also worth noting: According to Morgan Stanley, CPI forecasts for January are the furthest off-the-mark than for any other month of the year.

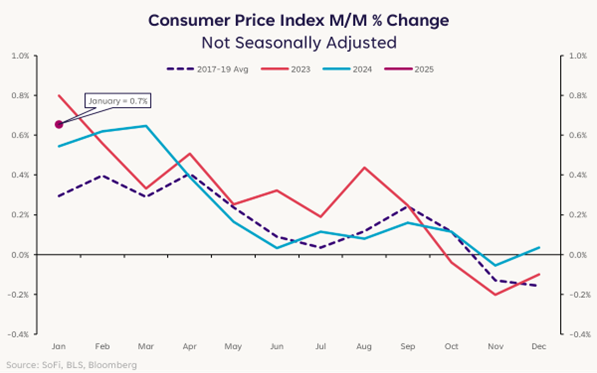

To play devil’s advocate on today’s market reaction, we think it’s important to point out the pattern that was evident pre-pandemic, and has been consistent over the past two years as inflation has gone through a normalization process. We’re using not seasonally adjusted data to get a look at the raw readings without any interference from smoothing or adjustments (which don’t seem to entirely remove seasonal forces anyway).

There is a case to be made for the “January effect,” which suggests that the first reading of the year typically comes in hot and tends to drop as the year progresses.

Some may call this hopeful, and perhaps it is. The main point being, it’s too soon to freak out and declare that inflation is in fact a major problem again. More importantly, January data tends to cause more freak outs than other months and we should be mindful of that possibility here.

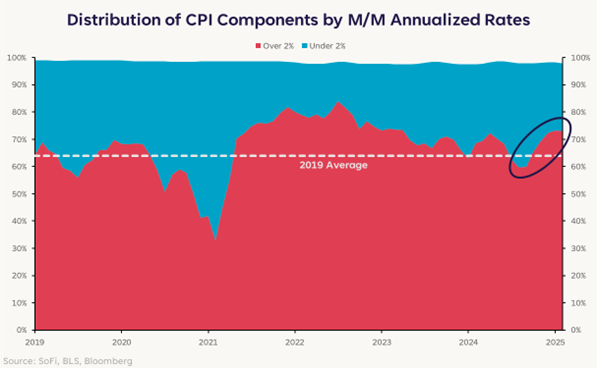

In the coming months, what we’ll be watching is this: What proportion of CPI components are a problem? In other words, how much of the index is still above the 2% target and is that group growing or shrinking?

Since summer 2024, that proportion has grown to 73% of components showing readings above 2%, compared with 60% in July of 2024. Obviously, we want to see this number fall, not rise. But if the proportion of components with problematic inflation readings continues to rise, the Fed and the economy could end up in a very tough spot.

Threshold for Pain

With all of the cross-currents in markets and the unknowns of trade politics, We believe the most important question investors need to ask themselves right now is, “what is my threshold for pain?” We say that because volatility in stocks and bonds is likely here for a while, as is volatility surrounding expectations for Fed policy.

That said, most economic fundamentals are solid and there is no obvious or glaring reason to expect that to change at this point. Earnings have come in generally strong for S&P 500 companies thus far, although company outlooks have been more muted and cautious, causing some negative market reactions. Investors are weary of the future, both in the near- and long-term, but the concrete results remain supportive.

The days of consistent risk-on multiple expansion are likely behind us given the uncertainty that remains. Portfolios should be diversified among asset classes, including asset classes that can dampen volatility such as cash, gold, and defensive sectors. In a higher for longer rate environment – which seems to look longer every month – valuations should be taken into account as a diversifying element as well. But this is not a signal to run for the hills, this is a warning that we need to keep our antennae up for the major risks that could derail a bull market. We don’t believe this bull is derailed… yet.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, investment advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.