Investment Strategy View: Learning from Earnings

Estimated reading time: 5 minutes

Triumphant Returns

A common plot device in books, movies and video games is that of failure and difficulty. The protagonist often runs into an obstacle that they initially can’t get past. They spend time developing and working out their issues, before eventually overcoming their challenge.

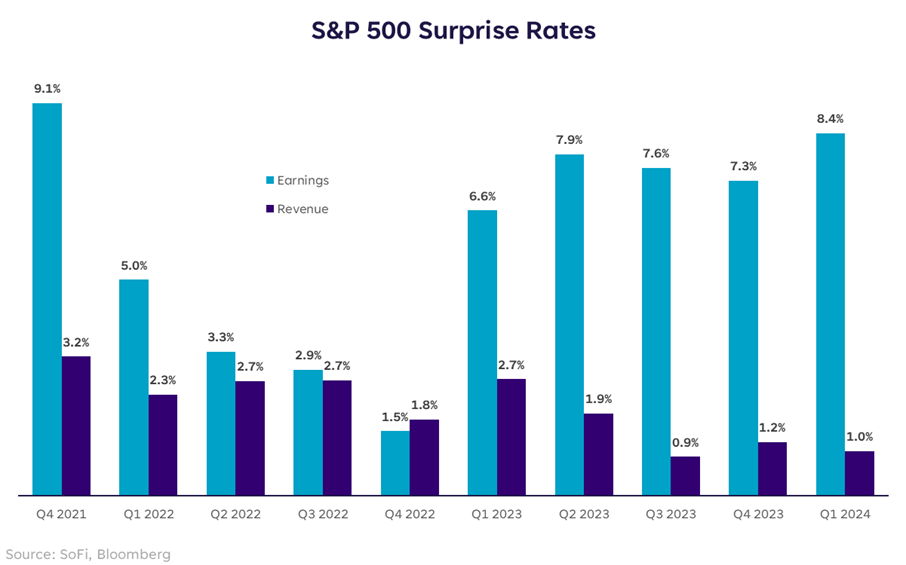

S&P 500 companies went through such a struggle a year ago – earnings growth was negative from the fourth quarter of 2022 until the second quarter of 2023 – but there were some positive signs underneath the surface. It was around that time that the earnings surprise rate increased dramatically, and it’s important to remember that markets are forward-looking and price in available information.

Earnings alone don’t move stock prices, it’s how those results compare to investors’ expectations that drive price action. Even though the going got tough, companies showed that they could hang in there despite the headwinds.

In the latest quarter, earnings results came in 8.3% above consensus, the biggest outperformance since the fourth quarter of 2021. It’s interesting to note then, that the revenue surprise rate stood near multi-year lows at 1.0%. This tells us that unexpected margin strength has driven the boost in profitability.

Widening Margins

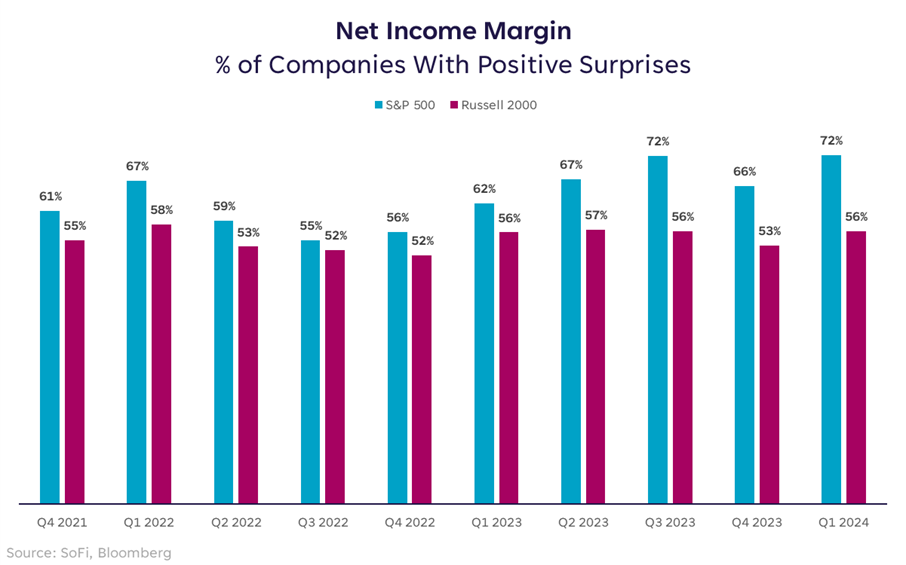

The margin story hasn’t been felt equally throughout the market though. While a growing share of S&P 500 companies (i.e. large-caps) have seen their net income margins beat expectations, Russell 2000 companies (i.e. small-caps) have not fared as well.

There isn’t any one explanation for why this has happened, but larger companies generally have been better positioned in the current macro environment. For one, the beneficiaries of the artificial intelligence theme have generally been large tech companies, as they’re the ones investing hundreds of billions into the technology. More broadly, however, the current high interest rate environment has a disproportionately negative effect on small-caps, as they tend to have shorter-term borrowings (i.e. inverted yield curve and higher short-term rates mean higher borrowing costs), more floating rate debt (i.e. higher fed funds rate raises borrowing costs rapidly), and lower credit ratings (i.e. lower quality raises borrowing costs).

Can David Beat Goliath?

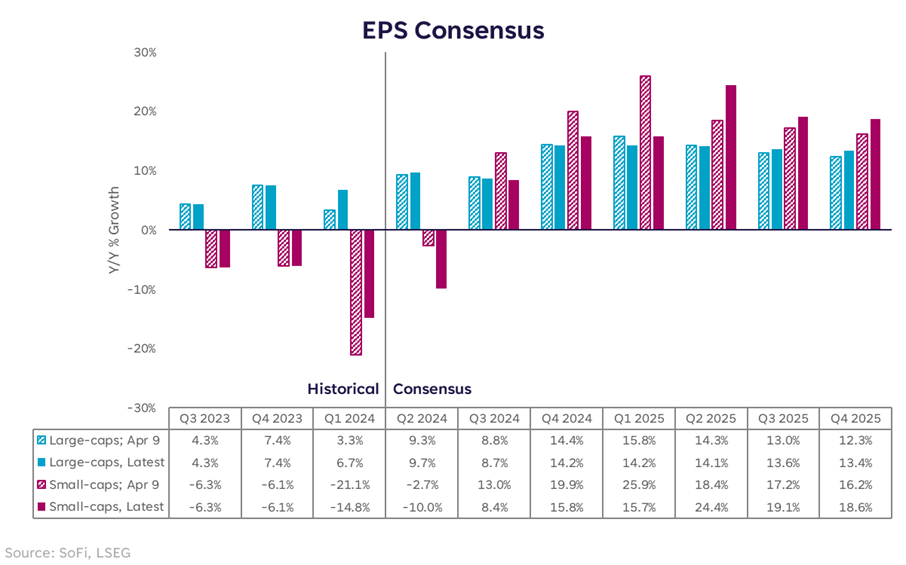

Analysts have taken note of this dynamic, with revisions to the outlook differing for large and small companies despite strong beats from both. Compared to the start of earnings season, growth expectations for larger companies are relatively unchanged. Small-caps, however, are expected to show significantly worse earnings growth over the next four quarters than was expected before companies started reporting.

In a sense, analysts are saying that while both groups surprised positively, large companies’ results are more durable while there is doubt that small-caps are ready to emerge from their now six quarter long earnings recession. There might be a light at the end of the tunnel though, as earnings growth is expected to finally get back in positive territory in the third quarter.

While protagonists sometimes emerge all on their own, they often need some help. The same might be true for small-caps: They certainly could emerge in this environment and outperform large-caps, but it would be hard for that to happen if the macro backdrop doesn’t shift. Some developments that would probably help small-caps relative to large-caps would be the Federal Reserve cutting interest rates – absent meaningful economic weakness – or some air coming out of the AI theme that could allow small-caps to catch-up.

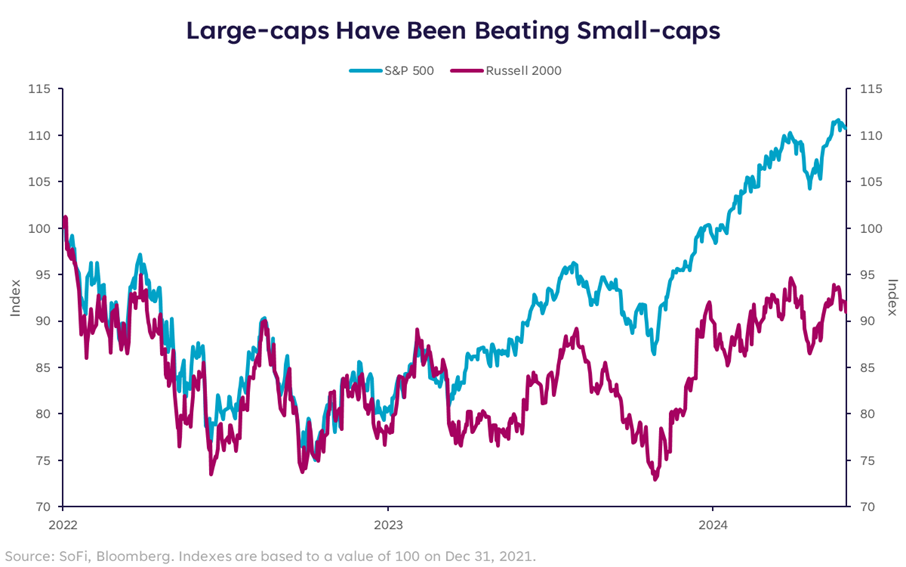

Until those broader macro forces shift, it’s likely that large-caps continue to be the winners in this David versus Goliath competition. But things could change later this summer if rate cuts come into focus. Don’t count David out just yet.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, investment advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.